The correction that began in February picked up steam in March, as the S&P 500 Total Return Index declined -4.98% for the month and brought its year-to-date return to -4.33%. The MarketVector™-GammaRoad U.S. Equity Strategy Index (Bloomberg: MVGMMA Index) entered March with only one of its three measures bullish for equity exposure. The price direction measure, which gauges the market’s overall price trend, turned bearish towards the end of the month. This caused the strategy to exit its remaining equity exposure and reallocate to 100% T-Bills exposure. As a result, the strategy declined by a more modest -2.83% in March, which brought its year-to-date return to -1.88%.

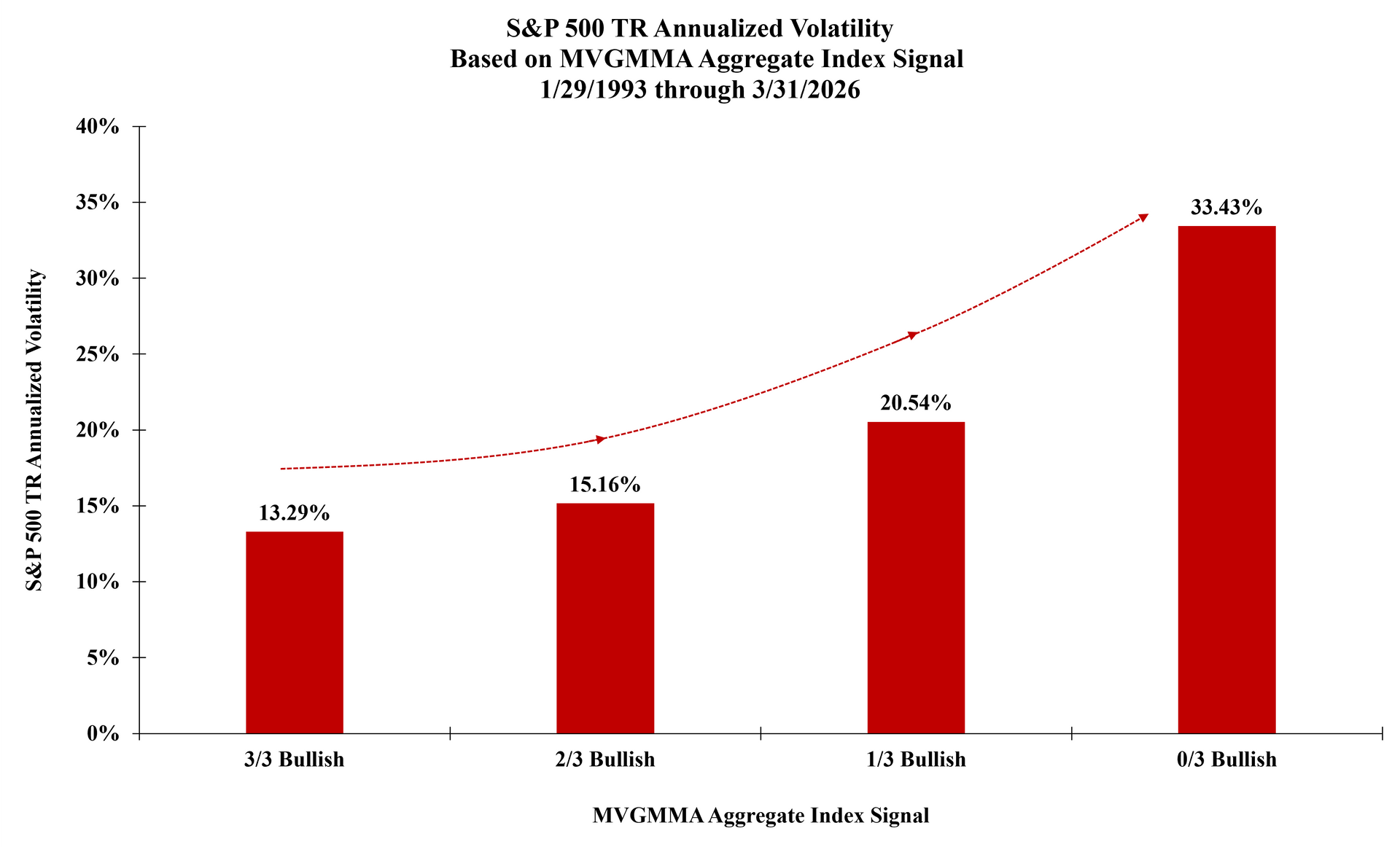

As we have noted through several prior monthly updates, we expect market conditions may be more susceptible to a meaningful increase in volatility when only one out of three measures is bullish. This expectation is even more pronounced when all three measures are bearish, i.e. when the strategy’s Aggregate Index Signal equals zero, where it sits at the time of this writing.

The following chart provides our basis for this higher expected volatility. The chart shows the annualized volatility for the S&P 500 Total Return Index’s daily returns since the base date of the MVGMMA Index, categorized by the level of the MVGMMA’s Aggregate Index Signal.

We chose January 29, 1993 as the base date for the MVGMMA Index so that the full research period would coincide with the inception of the SPDR® S&P 500® ETF Trust (“SPY”), which has the longest history amongst the largest and most liquid ETFs that passively track the S&P 500 Index.

Source: GammaRoad Capital Partners, LLC. This chart depicts the annualized volatility for the S&P 500 TR Index through points in time during which the MVGMMA Aggregate Index Signal was at each of its possible levels. The MVGMMA Index launched on December 22, 2023. Prior to December 22, 2023, all data points shown herein reflect periods when the MVGMMA Index was not actually published. Past performance is not indicative of future results. Please see the important disclosures that are integral to understanding the limitations applicable to the quantitative information in the presentation.

The End of Military Hostilities Does Not Eliminate the Persistence of Market Risks

Last month we shared our thoughts on several dominant market risk themes, including:

- The potential inflationary impulse from developing supply shocks in energy and agriculture due to the conflict in the Middle East;

- The public market’s repricing of private credit managers, their publicly traded portfolios, and the associated illiquidity risk; and

- The market’s shifting sentiment towards industries perceived as increasingly vulnerable to AI disruption, particularly software.

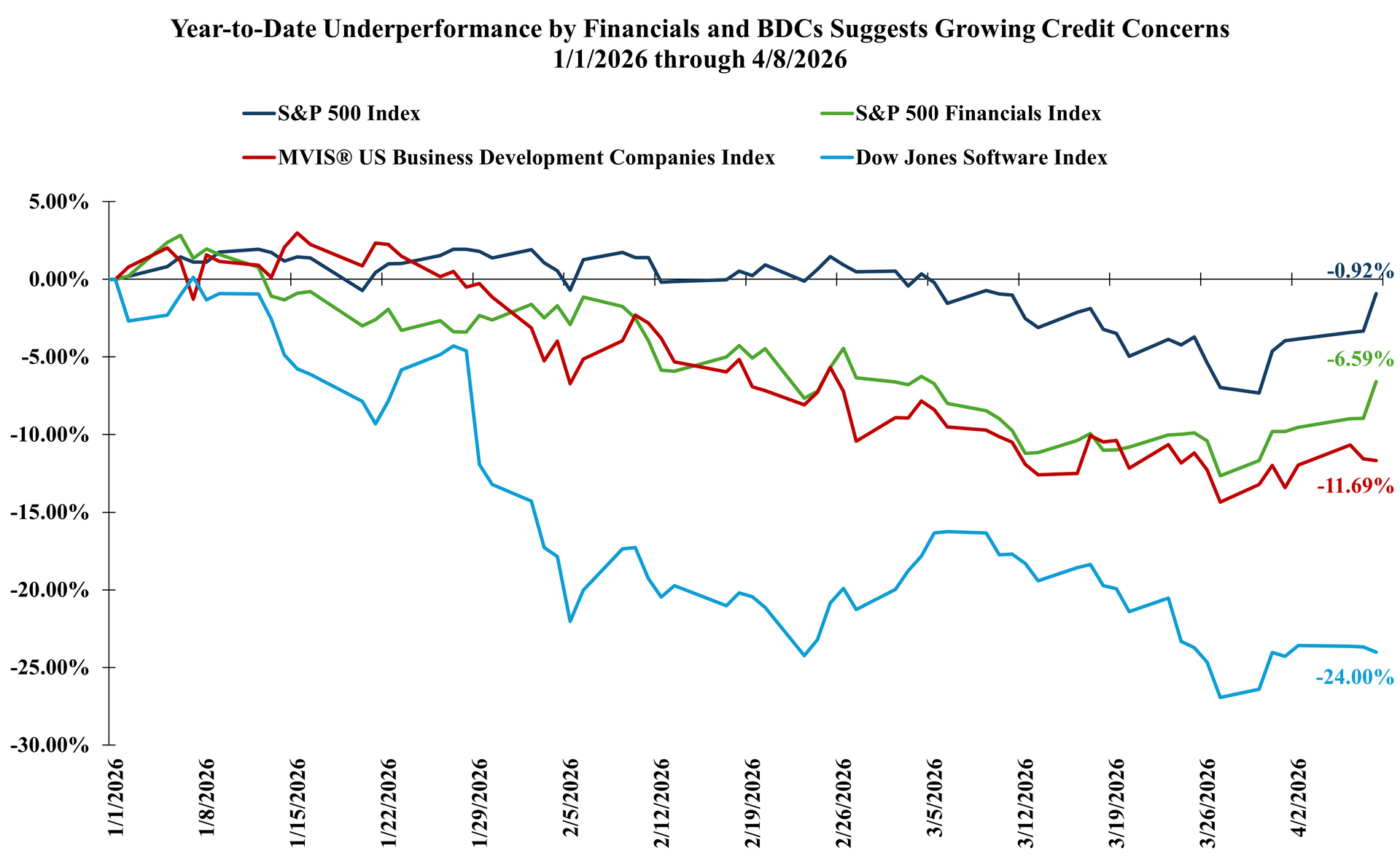

Regarding the latter two risk themes, the price weakness we noted last month for publicly listed banks, credit managers, and BDCs continued to indicate deterioration in loan books and underlying asset values through March and into early April, as shown in the chart below:

Source: GammaRoad Capital Partners, LLC. Past performance is not indicative of future results. Please see the important disclosures that are integral to understanding the limitations applicable to the quantitative information in the presentation.

The private credit and AI disruption risk themes certainly have not gone away, rather they have accelerated and (understandably) just taken somewhat of a back seat in media coverage to the war. As the conflict has evolved, we see that the damage already inflicted upon energy production and storage facilities, core inputs for crop fertilizer and for the petrochemical industry, and the related shipping challenges all have the potential to drive persistent inflationary pressures even after the military conflict finally abates.

The time-related uncertainty surrounding the recovery for these areas will then become a key influence over inflation risk and its persistence. The list of known unknowns in this regard is daunting to say the least:

- To what degree will the fractured nature of Iran’s military command compound the challenge of maintaining the potentially fragile ceasefire?

- How long will it take to complete repairs and restart production at damaged energy facilities?

- How much time will insurance underwriters require to see stability before they can price transit risk through the Strait of Hormuz and nearby regional waters?

- Will Iranian authorities continue to assess hefty toll fees on vessels that are permitted to sail through the Strait of Hormuz?

- How deeply will crop fertilizer inventories be depleted, how long might fertilizer applications be delayed, and how high will food prices rise due to lower yields?

- To what degree will the oil supply shock impact the petrochemical industry, which factors into the cost of almost any packaged item purchased at the supermarket?

Why Monetary and Fiscal Stimulus, If Needed, May Be More Constrained

Market participants have come to expect that if asset prices take a significant turn for the worse and the economy falters, then the central bank and the federal government will simply stimulate enough to rescue markets and fuel the next rally. The enormous monetary and fiscal policy responses to the Global Financial Crisis and the Global Pandemic certainly went a long way to cementing this expectation. However, just as we cautioned last month against treating all geopolitical events as a homogenous group, here we see a crucial difference in the unfolding Middle East conflict versus the GFC and the pandemic.

Specifically, the collapse of the residential real estate market and the resulting severe economic decline during the GFC were entirely deflationary in nature. Likewise the drastic economic shutdown during the global pandemic was entirely a deflationary event. The threat of outright deflation provided cover for monetary and fiscal policymakers to stimulate with tremendous magnitude. Liquidity can be used to address potential solvency problems when the prevailing conditions are deflationary.

By contrast the conflict today is markedly more inflationary in nature. The combination of higher energy and agricultural prices, food packaging costs and other petrochemical products, increased military spending, and growing political pressure to mitigate the affordability crisis, all suggest that the Federal Reserve in particular may face much greater constraints in providing stimulus relative to previous episodes.

What the Strategy’s Positioning Might Mean in the Current Environment

The confluence of the war’s inflationary implications with the deterioration in private credit and concerns over AI disruption potentially exacerbates the equity market’s vulnerability to a deeper drawdown. That said, we always want to emphasize that our framework does not aim to provide a market forecast. Instead, the MVGMMA Index seeks to provide an objective, continuous, diagnostic assessment of U.S. equity market risk at any point in time. This is why we frequently characterize the process as a nowcast rather than a forecast.

The strategy’s 100% allocation to T-Bills entering April suggests that the current market environment is commensurate with the least favorable conditions for U.S. equity exposure, when viewed through the lens of the MVGMMA Index’s three risk measures. If market conditions improve significantly from here, we expect the strategy’s unbiased, systematic process to respond accordingly and increase equity exposure. If instead the market correction deepens, the strategy is positioned to deliver on its objective and reduce portfolio risk when it is needed most.

For a refresher on the strategy’s architecture and underlying process, please

watch our video here.

Important Disclosures

THIS PRESENTATION AND THE INFORMATION CONTAINED HEREIN WAS PREPARED BY GAMMAROAD CAPITAL PARTNERS, LLC (“GAMMAROAD”) AND IS SUBJECT TO AND QUALIFIED BY THE IMPORTANT DISCLOSURES BELOW.

Confidential

This presentation is directed solely to existing and potential users of the MarketVector™-GammaRoad U.S. Equity Strategy Index (Bloomberg: MVGMMA Index,

“MVGMMA Index”) and is furnished on a confidential basis only for the use of the recipient and only for discussion purposes. This presentation and its contents are proprietary information of GammaRoad and may not be reproduced or otherwise disseminated in whole or in part without GammaRoad’s prior written consent.

Not Advice or Recommendation

This presentation is neither advice nor a recommendation to enter into any transaction. This presentation is for information, illustration and discussion purposes only and is not intended as an offer to buy or sell, nor a solicitation of an offer to buy or sell, any security, commodity or other financial instrument. Nothing contained in this presentation is intended to represent the rendering of accounting, tax, legal, regulatory or investment advice by GammaRoad. While investors should understand and consider the risks associated with making an investment decision, this presentation should not be relied upon for that purpose and should not be a basis of any investment decision or retention of the MVGMMA Index. This presentation and the MVGMMA Index do not take into account the particular investment objectives, financial circumstances, restrictions, particular needs or financial, accounting, regulatory, legal or tax situation of any particular person, investor or type of investor. Neither GammaRoad nor its principals, officers, employees or associated funds or entities (all of the foregoing collectively, “Related Persons”) hereby makes any representation to any person or entity as to the suitability of the MVGMMA Index or any investments nor provide advice or recommendations regarding an investor’s decision to allocate funds based on the use of the MVGMMA Index or to maintain or sell investments based on the MVGMMA Index.

An investment decision by you to employ the MVGMMA Index in any capacity should be based on your independent judgment and customary and thorough due diligence procedures, including consultation with your own professional tax, legal and investment advisors. You should also inform yourself as to: (1) the legal requirements within your jurisdictions for the purchase, holding or disposal of investments; and (2) any income and other taxes which may apply to the purchase, holding and disposal of investments. Furthermore, you should keep in mind that any subsequent change in facts or circumstances could materially affect the accounting, tax, legal or regulatory treatment consequences of the MVGMMA Index and investments. Before you make any investment decisions based on the MVGMMA Index, you should determine whether the investment is suitable for you in light of your circumstances, investment objectives, financial situation and risk tolerance.

GammaRoad is not an Advisor or a Fiduciary

GammaRoad is not and does not purport to be an advisor as to legal, taxation, accounting, financial or regulatory matters in any jurisdiction. GammaRoad is not registered with any federal or state regulator and no fiduciary relationship under federal and/or state securities laws, the Commodity Exchange Act and/or ERISA is created by investing based on the MVGMMA Index, or through any communication with GammaRoad.

Limitation on Liability

No liability whatsoever is accepted for any loss (whether direct, indirect, or consequential) that may arise from any use of the information contained in or derived from this presentation or by use of the MVGMMA Index. In addition, GammaRoad, disclaims any and all liability as to the completeness or accuracy of the information contained herein and for any omissions of material facts. However, nothing herein shall in any way constitute a waiver or limitation of any rights available under applicable federal or state laws.

MVGMMA Index is Subject to Change

Please reference the MVGMMA Index Guide at www.marketvector.com/rulebooks/download/MVGMMA_Index_Guide.pdf for information regarding the development of the MVGMMA Index, its methodology and its risk management techniques.

Any changes to the Index Guide will be reviewed and approved by MarketVector Indexes (“MarketVector”) and MarketVector’s Legal and Compliance Department. MarketVector’s Legal and Compliance Department may also request a conclusive description and further information on any change and may consult MarketVector’s operations department on such changes. The key elements to be analyzed in this phase of the change process are robustness, transparency, reliability and integrity. The result of the review will be communicated to MarketVector’s operations department. The email will be archived by MarketVector’s operations department.

Changes that might immediately change the composition of the MVGMMA Index or must be considered material for any other reason also need to be approved by MarketVector’s Independent Oversight Function (“IOF”) prior to their publication and implementation.

In case of material changes an advance notice will be published and provided to users by MarketVector. MarketVector will generally disseminate a notification related to an Index Guide change 30 days prior to the change. A shorter period of time may be applied at MarketVector’s discretion if the relevant index has not been licensed for a financial product to a third party. The notice will describe a clear time frame that gives the opportunity to analyze and comment upon the impact of such proposed material change. Any material comments received in relation to the Index Guide change and MarketVector’s response to those comments will be made publicly accessible after any consultation, except where confidentiality has been requested by the originator of the comments.

Investment Performance

All performance information reflects the performance of the MarketVector™-GammaRoad U.S. Equity Strategy Index and does not reflect the trading of an actual account. The MVGMMA Index launched on December 22, 2023. Prior to December 22, 2023, all performance shown herein reflects backtested information based on the application of the MVGMMA Index methodology to the SPDR® S&P 500® ETF Trust (“SPY”) and the ProShares Ultra S&P500® (“SSO”) price and dividend data for the MVGMMA Index’s equity component during periods when the MVGMMA Index was not actually published. Prior to the inception of the SSO, the performance exhibits use twice the daily return of the SPY minus the daily equivalent of the SSO’s total expense ratio. For the non-equity component of the MVGMMA Index, the performance exhibits use the daily return and dividends for the SPDR® Bloomberg 1-3 Month T-Bill ETF (“BIL”). Prior to the inception of the BIL, the performance exhibits use a cash return that is the daily equivalent of the market yield on U.S. Treasury Securities at 3-Month Constant Maturity minus the daily equivalent of the BIL’s total expense ratio. The slides that show target equity weight changes apply the MVGMMA Index methodology to the S&P 500 Index price data during the periods shown. Both the S&P 500 TR and the S&P 500 Index (collectively the “S&P 500 Indices”) are indices comprised of the same 500 stocks chosen from all major industries based on market size, liquidity and industry grouping, among other factors. The difference between the S&P 500 TR and the S&P 500 Index is that the S&P 500 TR reflects the reinvestment of dividends while the S&P 500 Index does not. Investments cannot be made directly in broad-based securities indices. Therefore, the application of the MVGMMA Index methodology to the S&P 500 Indices is for illustration purposes only to demonstrate the efficacy of the MVGMMA Index methodology applied to these indices. January 29, 1993 was chosen as the base date for the MVGMMA Index so that the full research period would coincide with the inception of the SPDR® S&P 500® ETF Trust (“SPY”), which has the longest history amongst the largest and most liquid ETFs that passively track the S&P 500 Index. Additional information about the S&P 500 Indices and the U.S. Treasury Securities at 3-Month Constant Maturity is available from GammaRoad upon request.

The investment performance shown includes the reinvestment of dividends, interest and capital gains according to the MVGMMA Index and there was no withdrawal of cash during the performance period. In addition, you may pay brokerage commissions, exchange fees, and clearing fees to execute the MVGMMA Index methodology, none of which are subtracted in calculating the back-tested performance shown. Differences in the methodology used to calculate performance may also lead to different performance results than those shown. Annualized total return is computed on a compounded monthly basis. Volatility (standard deviation) and maximum drawdown percentage are computed on a daily basis. Beta and skew are computed on a monthly basis.

Back-tested performance is a type of hypothetical performance that cannot completely account for the impact of financial risk in actual management of a portfolio. In fact, there can be sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular investment strategy due to many factors, some of which are described below. For example, the ability to withstand losses and adhere to the MVGMMA Index methodology in spite of trading losses is unknown and could have adversely affected actual results. Furthermore, back-tested performance results are prepared with the benefit of hindsight. This means that the MVGMMA Index has been formed in the present based in part on application of the MVGMMA Index methodology to the SPY, SSO, and BIL ETFs during the back-tested periods. The MVGMMA Index may have been constructed differently if GammaRoad did not have the benefit of its current hindsight and the MVGMMA Index may have performed significantly worse than the performance reflected herein. Furthermore, if the MVGMMA Index changes, the back-tested performance shown is not indicative of how the MVGMMA Index will perform if these changes occur. In addition, as noted above the back-tested performance shown does not subtract any brokerage commissions, exchange fees, and clearing fees. For the foregoing reasons and for numerous other reasons related to the markets, no representation is made that any investor using the MVGMMA Index will or is likely to achieve profits or losses similar to those shown.

Performance may vary substantially from year to year or even from month to month. Differences in the timing of transactions and market conditions prevailing at the time of investment may lead to different results. The value of investments can go down as well as up. Past performance is not indicative of future results and GammaRoad makes no representation that any user of the MVGMMA Index will or is likely to achieve profits or losses similar to those shown herein.

Benchmark Comparison

The performance shown is compared to the S&P 500 TR. The comparisons to the S&P 500 TR are included merely to show the general performance in the market in the periods indicated and is not intended to imply that the MVGMMA Index is similar to the S&P 500 TR in either composition or element of risk. Investments cannot be made directly in a broad-based securities index.

Risk of Loss and Other Risks

Investing in securities entails certain risks, including the possible loss of the entire principal amount invested. Volatility and returns depend on a variety of factors including overall market conditions, and unpredictable economic and political events.

All projections, valuations, and statistical analyses are provided to assist the recipient in the evaluation of the matters described herein. Such projections, valuations and analyses may be based on subjective assessments and assumptions and may use one among many alternative methodologies that produce different results; accordingly, such projections, valuations and statistical analyses should not be viewed as facts and should not be relied upon as an accurate prediction of future events.

Investments pursuant to the MVGMMA Index may be exposed to risks relating to non-U.S. markets, including, without limitation, risks relating to currency exchange, tax, lack of liquidity, market manipulation, political instability and higher transaction costs.

No representation is made that the MVGMMA Index's investment processes, investment objectives, goals or risk management techniques will or are likely to be achieved or successful, or that the MVGMMA Index methodology and/or any investment will make any profit or will not sustain losses. The MVGMMA Index may not be suitable for everyone.

Conflicts of Interest

GammaRoad’s Related Persons may invest personal assets pursuant to the MVGMMA Index methodology. To address potential conflicts of interest with the investing of users of the MVGMMA Index, GammaRoad has instituted an internal Personal Trading Policy with which all Related Persons are required to comply. With respect to each GammaRoad strategy, GammaRoad’s Personal Trading Policy seeks to allow users to have the opportunity to trade before and at better prices than Related Persons. A copy of GammaRoad’s Personal Trading Policy is available upon request.

Limitations on Information Contained Herein

This presentation is based on information including, but not limited to third-party benchmark information, that has been obtained from sources that GammaRoad believes to be reliable; however, such information has not been independently verified. GammaRoad (i) makes no representation as to, and accepts no responsibility or liability for, the accuracy, truthfulness or completeness of the information; (ii) and does not represent it as accurate, true or complete; (iii) makes no warranty, express or implied regarding it; and (iv) shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use unless the waiver of such liability constitutes the waiver of any rights you may have under applicable federal or state laws.

The information in this presentation is current as of the date indicated and is subject to change or amendment. The delivery of this presentation at any time does not imply that the information contained herein is correct at any time subsequent to such date. GammaRoad undertakes no responsibility or obligation to revise or update this presentation and/or the opinions, statements, assumptions, analyses, assessments, projections, forward looking statements, similar statements and other views expressed in this presentation (collectively, the “Statements”). All Statements constitute only subjective views of GammaRoad, should not be relied on, and are subject to change without notice due to many factors, including fluctuating market conditions, and economic factors.