May 2026 delivered another rewarding month for U.S. equity investors as the S&P 500 Total Return Index rose +5.26%, which brought its year-to-date return to +11.27%. The MarketVector™-GammaRoad U.S. Equity Strategy Index (Bloomberg: MVGMMA Index) maintained its positioning through May at roughly 2/3rd equity exposure and 1/3rd T-Bills exposure based on its three underlying market risk measures. The strategy returned +3.63% in May, which brought its year-to-date return to +4.26%.

As the rebound rally continued through May, we observed increased attention and market narrative focusing on the potential inflationary implications stemming from the Middle East conflict. We introduced this theme in our March update, and then outlined a series of questions in our April update exploring how the persistence of these inflationary pressures might constrain the ability of monetary policy and fiscal policy to alleviate any economic tightening that ensues later this year.

The bond market has certainly taken notice that these inflationary pressures may be increasingly durable. Since the war began, the U.S. 10-Year Treasury yield has risen 0.57% through June 5th. Growth expectations have remained fairly stable, thus it seems reasonable that inflation expectations have been the primary marginal influence for this recent rise at the long end of the curve.

Given the healthy risk appetite on display from equity investors over the last two months, it is no surprise to see an increasing chorus of the bullish cheer that “Rising rates are not a worry for the stock market.”

We have seen multiple versions of this assertion in recent weeks across financial media and public forums. Remarkably, every version we have seen offers a rather limited view of market history to support this statement.

As we will now demonstrate, we would urge investors to be very careful of the time period chosen to support market expectations.

To explore the validity of the suggestion that “rising rates do not matter”, we must first define how we will measure “rising” and “falling”. Here we will simply use the rudimentary 12-month average yield on a rolling basis to capture whether the yield is rising or falling over time.

Then to capture equity returns we will measure the annualized returns for the S&P 500 Index (price only) through all periods when the 12-month average Treasury yield is rising or falling versus the prior month.

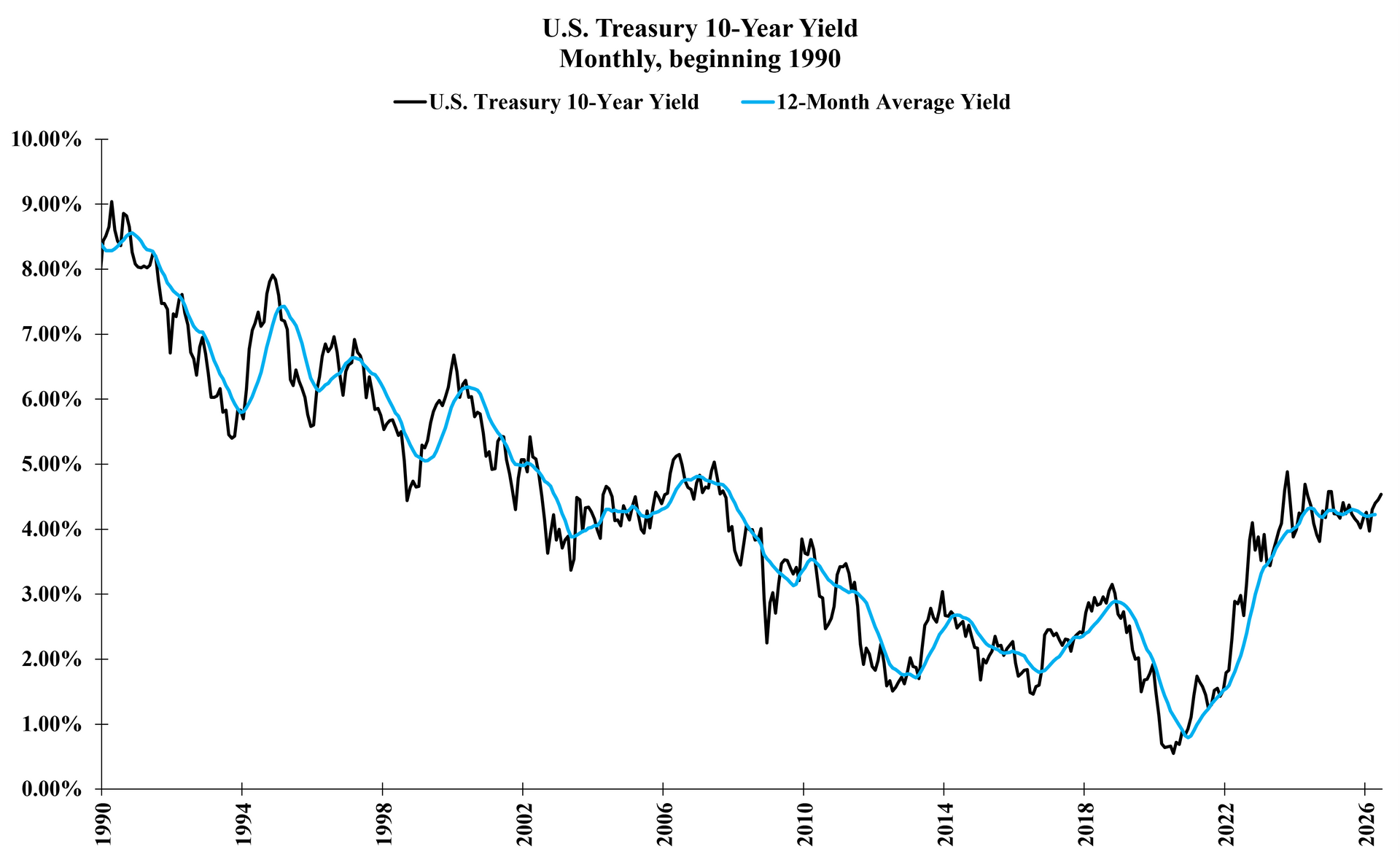

Let’s first explore the market history beginning with the year 1990, as we have often seen used for the “rates don’t matter” assertion. The monthly yield history and its 12-month average look like this:

Source: Federal Reserve Bank of St. Louis, GammaRoad Capital Partners, LLC. Past performance is not indicative of future results. Please see the important disclosures that are integral to understanding the limitations applicable to the quantitative information in the presentation.

The next chart shows the annualized return for the S&P 5oo Index (price only) when the 12-month average Treasury yield is falling versus when it is rising.

Source: Federal Reserve Bank of St. Louis, GammaRoad Capital Partners, LLC. Past performance is not indicative of future results. Please see the important disclosures that are integral to understanding the limitations applicable to the quantitative information in the presentation.

Hallelujah! Rates do not matter! In fact, stocks have annualized at a much higher clip when the 10-year Treasury yield is trending higher. Case closed.

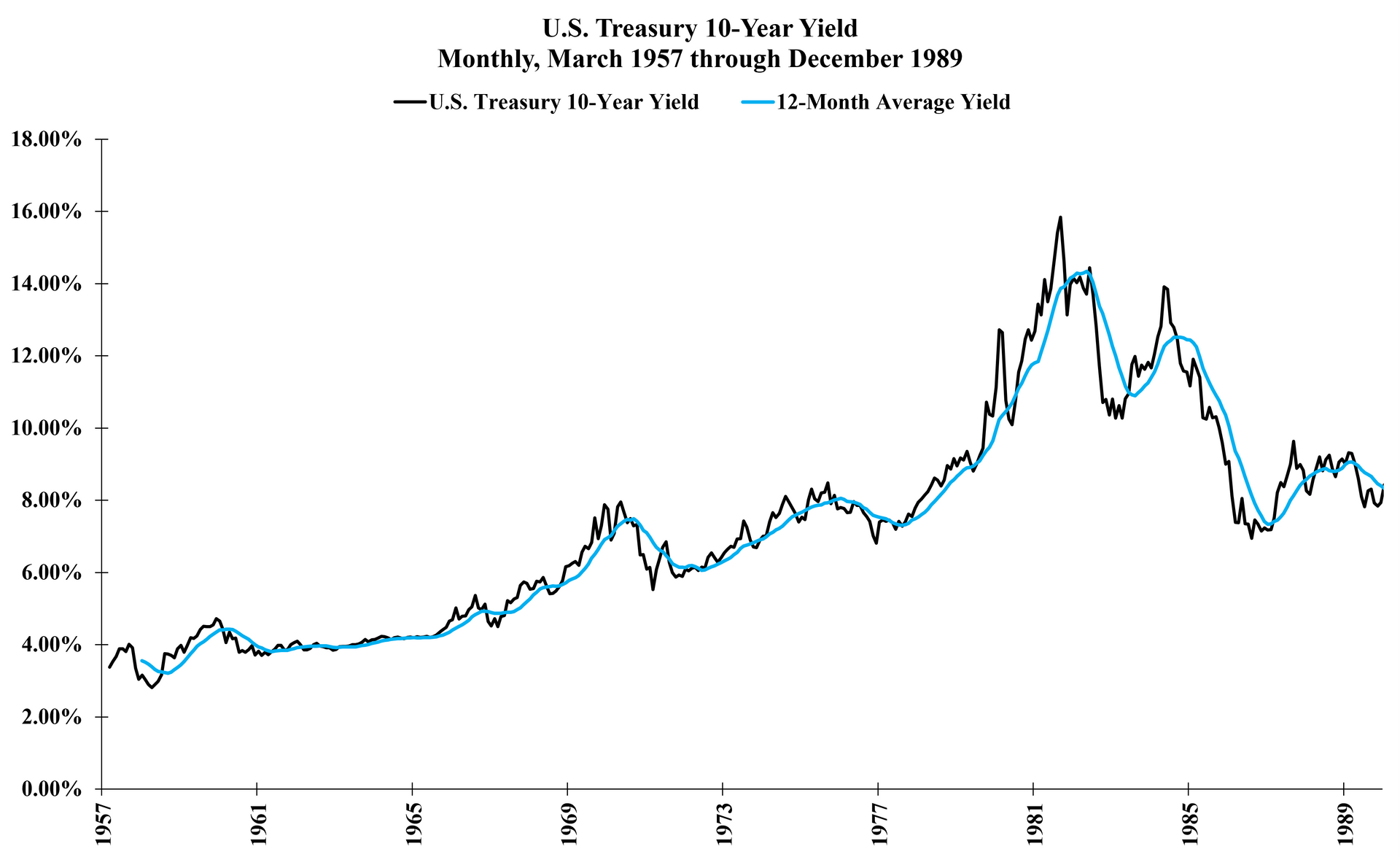

Fortunately we have far more extensive market history available for us to explore further. Let’s extend the picture of the 10-year Treasury yield and its simple trend back to March 1957. We have deliberately chosen this starting point to coincide with the month that the S&P 500 Index was first published with 500 constituents. Here is what the yield history looks like before 1990:

Source: 10-Year Yield 1957 through 1961 sourced from Swinkels, Laurens. 2025. “Historical Data: International Monthly Government Bond Returns.” DataverseNL. https://doi.org/10.34894/YWT2IX. 10-Year Yield beginning 1962 sourced from Federal Reserve Bank of St. Louis, GammaRoad Capital Partners, LLC. Past performance is not indicative of future results. Please see the important disclosures that are integral to understanding the limitations applicable to the quantitative information in the presentation.

This is quite a different picture than the earlier chart that begins in 1990. These two charts provide a valuable reminder that interest rate cycles can last for decades. The choice to begin the “rates don’t matter” statement with 1990 (or even 2000 as we have also seen) does not capture the historical context for the prevailing interest rate trend in any meaningful way.

A simple look at either yield history chart shows two distinctly evident trends: the secular rise in rates during the 1960s and 1970s, and the secular decline in rates from the early 1980s through 2021.

We also encourage investors to exercise caution over the return measurement chosen for the “rates don’t matter” statement. Many published opinions we have seen employ some form of average returns (e.g. average monthly returns, average annual rolling returns). Looking at average returns at single points in time does not offer any useful assessment. This is because, like most market influences, it is the trend in the influence that matters far more than the level at any point in time.

This is the reason we choose to examine the annualized returns based on the prevailing yield trend over time. The pictures above of the 10-year yield history reveal that the choice to only use market data during a single, secular trend amounts to good old-fashioned cherry-picking, whether intentional or not.

Let’s continue the analysis with some cherry-picking of our own, and look at the period spanning 1966 – 1981, which captures a well-known secular equity bear market characterized by rising rates and persistent inflationary pressures. Here is the chart showing the annualized returns for the S&P 5oo Index (price only) when the 12-month average yield is rising versus when it is falling during this polar-opposite yield regime:

Source: Federal Reserve Bank of St. Louis, GammaRoad Capital Partners, LLC. Past performance is not indicative of future results. Please see the important disclosures that are integral to understanding the limitations applicable to the quantitative information in the presentation.

Whoops. Maybe rising rates do matter after all. To remove the cherry-picking and incorporate the full market history, let’s now examine the annualized returns during the full period March 1957 through May 2026. We will include all three periods for comparison: the falling rate regime of recent decades, the rising rate regime of the previous secular cycle, and the full extended period beginning March 1957:

Source: Federal Reserve Bank of St. Louis, GammaRoad Capital Partners, LLC. Past performance is not indicative of future results. Please see the important disclosures that are integral to understanding the limitations applicable to the quantitative information in the presentation.

This full period for the S&P 500 Index price history nicely includes multiple bull and bear market cycles over a roughly 70-year period. The right side of the chart demonstrates that over the last seven decades, the prevailing trend in interest rates has clearly mattered to equity returns.

To test robustness and avoid the possibility of cherry-picking the averaging period used for the 10-year yield, the following chart summarizes the same results by varying the averaging period between 6 to 18 months.

Source: Federal Reserve Bank of St. Louis, GammaRoad Capital Partners, LLC. Past performance is not indicative of future results. Please see the important disclosures that are integral to understanding the limitations applicable to the quantitative information in the presentation.

The chart above reinforces the validity of the view that if rates are trending higher, expected equity returns should likely be lower. Note that while there are ample, well-documented fundamental reasons why equities should exhibit rate sensitivity, here we are simply testing the assertion that “rising rates are not a worry for the stock market” against seven decades of market evidence. An unbiased, objective analysis reveals the reality that rates do indeed matter to equities over time.

Naturally this view may receive pushback with numerous reasons why it’s different this time. Everyone knows that cliché because history has so consistently shown the danger of that thought process during every equity market cycle. Despite the heft of evidence shown in the charts above, we remain cognizant that the transformative and seemingly ubiquitous economic impact of AI introduces a bull market driver that potentially stands unique relative to history. Ironically this may turn out to be exactly why it’s not different this time at all. We are collectively watching in real-time as the persistence of inflationary cost pressures through energy and materials becomes increasingly critical to the AI capex story, which is possibly the single greatest driver for the current bull market and underlying economic growth.

None of this is intended to be a prediction. This month’s update offers a respectful expression of caution: perhaps it is dangerous to declare that “rates do not matter to equities” when the evidence so clearly suggests the contrary. We encourage all market participants to give careful thought to the time periods and prevailing conditions included in the data when assessing any such assertions.

The MVGMMA Index enters June with two of its three risk measures bullish. The strategy’s current positioning continues to provide for participation in further equity upside while remaining balanced with the duration-neutral cushion of T-Bills. If you believe that navigating market risk can benefit from an unbiased, rules-based approach, we invite you to

connect with us to learn more.

For a refresher on the strategy’s architecture and underlying process, please watch our video here.

Important Disclosures

THIS PRESENTATION AND THE INFORMATION CONTAINED HEREIN WAS PREPARED BY GAMMAROAD CAPITAL PARTNERS, LLC (“GAMMAROAD”) AND IS SUBJECT TO AND QUALIFIED BY THE IMPORTANT DISCLOSURES BELOW.

Confidential

This presentation is directed solely to existing and potential users of the MarketVector™-GammaRoad U.S. Equity Strategy Index (Bloomberg: MVGMMA Index,

“MVGMMA Index”) and is furnished on a confidential basis only for the use of the recipient and only for discussion purposes. This presentation and its contents are proprietary information of GammaRoad and may not be reproduced or otherwise disseminated in whole or in part without GammaRoad’s prior written consent.

Not Advice or Recommendation

This presentation is neither advice nor a recommendation to enter into any transaction. This presentation is for information, illustration and discussion purposes only and is not intended as an offer to buy or sell, nor a solicitation of an offer to buy or sell, any security, commodity or other financial instrument. Nothing contained in this presentation is intended to represent the rendering of accounting, tax, legal, regulatory or investment advice by GammaRoad. While investors should understand and consider the risks associated with making an investment decision, this presentation should not be relied upon for that purpose and should not be a basis of any investment decision or retention of the MVGMMA Index. This presentation and the MVGMMA Index do not take into account the particular investment objectives, financial circumstances, restrictions, particular needs or financial, accounting, regulatory, legal or tax situation of any particular person, investor or type of investor. Neither GammaRoad nor its principals, officers, employees or associated funds or entities (all of the foregoing collectively, “Related Persons”) hereby makes any representation to any person or entity as to the suitability of the MVGMMA Index or any investments nor provide advice or recommendations regarding an investor’s decision to allocate funds based on the use of the MVGMMA Index or to maintain or sell investments based on the MVGMMA Index.

An investment decision by you to employ the MVGMMA Index in any capacity should be based on your independent judgment and customary and thorough due diligence procedures, including consultation with your own professional tax, legal and investment advisors. You should also inform yourself as to: (1) the legal requirements within your jurisdictions for the purchase, holding or disposal of investments; and (2) any income and other taxes which may apply to the purchase, holding and disposal of investments. Furthermore, you should keep in mind that any subsequent change in facts or circumstances could materially affect the accounting, tax, legal or regulatory treatment consequences of the MVGMMA Index and investments. Before you make any investment decisions based on the MVGMMA Index, you should determine whether the investment is suitable for you in light of your circumstances, investment objectives, financial situation and risk tolerance.

GammaRoad is not an Advisor or a Fiduciary

GammaRoad is not and does not purport to be an advisor as to legal, taxation, accounting, financial or regulatory matters in any jurisdiction. GammaRoad is not registered with any federal or state regulator and no fiduciary relationship under federal and/or state securities laws, the Commodity Exchange Act and/or ERISA is created by investing based on the MVGMMA Index, or through any communication with GammaRoad.

Limitation on Liability

No liability whatsoever is accepted for any loss (whether direct, indirect, or consequential) that may arise from any use of the information contained in or derived from this presentation or by use of the MVGMMA Index. In addition, GammaRoad, disclaims any and all liability as to the completeness or accuracy of the information contained herein and for any omissions of material facts. However, nothing herein shall in any way constitute a waiver or limitation of any rights available under applicable federal or state laws.

MVGMMA Index is Subject to Change

Please reference the MVGMMA Index Guide at www.marketvector.com/rulebooks/download/MVGMMA_Index_Guide.pdf for information regarding the development of the MVGMMA Index, its methodology and its risk management techniques.

Any changes to the Index Guide will be reviewed and approved by MarketVector Indexes (“MarketVector”) and MarketVector’s Legal and Compliance Department. MarketVector’s Legal and Compliance Department may also request a conclusive description and further information on any change and may consult MarketVector’s operations department on such changes. The key elements to be analyzed in this phase of the change process are robustness, transparency, reliability and integrity. The result of the review will be communicated to MarketVector’s operations department. The email will be archived by MarketVector’s operations department.

Changes that might immediately change the composition of the MVGMMA Index or must be considered material for any other reason also need to be approved by MarketVector’s Independent Oversight Function (“IOF”) prior to their publication and implementation.

In case of material changes an advance notice will be published and provided to users by MarketVector. MarketVector will generally disseminate a notification related to an Index Guide change 30 days prior to the change. A shorter period of time may be applied at MarketVector’s discretion if the relevant index has not been licensed for a financial product to a third party. The notice will describe a clear time frame that gives the opportunity to analyze and comment upon the impact of such proposed material change. Any material comments received in relation to the Index Guide change and MarketVector’s response to those comments will be made publicly accessible after any consultation, except where confidentiality has been requested by the originator of the comments.

Investment Performance

All performance information reflects the performance of the MarketVector™-GammaRoad U.S. Equity Strategy Index and does not reflect the trading of an actual account. The MVGMMA Index launched on December 22, 2023. Prior to December 22, 2023, all performance shown herein reflects backtested information based on the application of the MVGMMA Index methodology to the SPDR® S&P 500® ETF Trust (“SPY”) and the ProShares Ultra S&P500® (“SSO”) price and dividend data for the MVGMMA Index’s equity component during periods when the MVGMMA Index was not actually published. Prior to the inception of the SSO, the performance exhibits use twice the daily return of the SPY minus the daily equivalent of the SSO’s total expense ratio. For the non-equity component of the MVGMMA Index, the performance exhibits use the daily return and dividends for the SPDR® Bloomberg 1-3 Month T-Bill ETF (“BIL”). Prior to the inception of the BIL, the performance exhibits use a cash return that is the daily equivalent of the market yield on U.S. Treasury Securities at 3-Month Constant Maturity minus the daily equivalent of the BIL’s total expense ratio. The slides that show target equity weight changes apply the MVGMMA Index methodology to the S&P 500 Index price data during the periods shown. Both the S&P 500 TR and the S&P 500 Index (collectively the “S&P 500 Indices”) are indices comprised of the same 500 stocks chosen from all major industries based on market size, liquidity and industry grouping, among other factors. The difference between the S&P 500 TR and the S&P 500 Index is that the S&P 500 TR reflects the reinvestment of dividends while the S&P 500 Index does not. Investments cannot be made directly in broad-based securities indices. Therefore, the application of the MVGMMA Index methodology to the S&P 500 Indices is for illustration purposes only to demonstrate the efficacy of the MVGMMA Index methodology applied to these indices. January 29, 1993 was chosen as the base date for the MVGMMA Index so that the full research period would coincide with the inception of the SPDR® S&P 500® ETF Trust (“SPY”), which has the longest history amongst the largest and most liquid ETFs that passively track the S&P 500 Index. Additional information about the S&P 500 Indices and the U.S. Treasury Securities at 3-Month Constant Maturity is available from GammaRoad upon request.

The investment performance shown includes the reinvestment of dividends, interest and capital gains according to the MVGMMA Index and there was no withdrawal of cash during the performance period. In addition, you may pay brokerage commissions, exchange fees, and clearing fees to execute the MVGMMA Index methodology, none of which are subtracted in calculating the back-tested performance shown. Differences in the methodology used to calculate performance may also lead to different performance results than those shown. Annualized total return is computed on a compounded monthly basis. Volatility (standard deviation) and maximum drawdown percentage are computed on a daily basis. Beta and skew are computed on a monthly basis.

Back-tested performance is a type of hypothetical performance that cannot completely account for the impact of financial risk in actual management of a portfolio. In fact, there can be sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular investment strategy due to many factors, some of which are described below. For example, the ability to withstand losses and adhere to the MVGMMA Index methodology in spite of trading losses is unknown and could have adversely affected actual results. Furthermore, back-tested performance results are prepared with the benefit of hindsight. This means that the MVGMMA Index has been formed in the present based in part on application of the MVGMMA Index methodology to the SPY, SSO, and BIL ETFs during the back-tested periods. The MVGMMA Index may have been constructed differently if GammaRoad did not have the benefit of its current hindsight and the MVGMMA Index may have performed significantly worse than the performance reflected herein. Furthermore, if the MVGMMA Index changes, the back-tested performance shown is not indicative of how the MVGMMA Index will perform if these changes occur. In addition, as noted above the back-tested performance shown does not subtract any brokerage commissions, exchange fees, and clearing fees. For the foregoing reasons and for numerous other reasons related to the markets, no representation is made that any investor using the MVGMMA Index will or is likely to achieve profits or losses similar to those shown.

Performance may vary substantially from year to year or even from month to month. Differences in the timing of transactions and market conditions prevailing at the time of investment may lead to different results. The value of investments can go down as well as up. Past performance is not indicative of future results and GammaRoad makes no representation that any user of the MVGMMA Index will or is likely to achieve profits or losses similar to those shown herein.

Benchmark Comparison

The performance shown is compared to the S&P 500 TR. The comparisons to the S&P 500 TR are included merely to show the general performance in the market in the periods indicated and is not intended to imply that the MVGMMA Index is similar to the S&P 500 TR in either composition or element of risk. Investments cannot be made directly in a broad-based securities index.

Risk of Loss and Other Risks

Investing in securities entails certain risks, including the possible loss of the entire principal amount invested. Volatility and returns depend on a variety of factors including overall market conditions, and unpredictable economic and political events.

All projections, valuations, and statistical analyses are provided to assist the recipient in the evaluation of the matters described herein. Such projections, valuations and analyses may be based on subjective assessments and assumptions and may use one among many alternative methodologies that produce different results; accordingly, such projections, valuations and statistical analyses should not be viewed as facts and should not be relied upon as an accurate prediction of future events.

Investments pursuant to the MVGMMA Index may be exposed to risks relating to non-U.S. markets, including, without limitation, risks relating to currency exchange, tax, lack of liquidity, market manipulation, political instability and higher transaction costs.

No representation is made that the MVGMMA Index's investment processes, investment objectives, goals or risk management techniques will or are likely to be achieved or successful, or that the MVGMMA Index methodology and/or any investment will make any profit or will not sustain losses. The MVGMMA Index may not be suitable for everyone.

Conflicts of Interest

GammaRoad’s Related Persons may invest personal assets pursuant to the MVGMMA Index methodology. To address potential conflicts of interest with the investing of users of the MVGMMA Index, GammaRoad has instituted an internal Personal Trading Policy with which all Related Persons are required to comply. With respect to each GammaRoad strategy, GammaRoad’s Personal Trading Policy seeks to allow users to have the opportunity to trade before and at better prices than Related Persons. A copy of GammaRoad’s Personal Trading Policy is available upon request.

Limitations on Information Contained Herein

This presentation is based on information including, but not limited to third-party benchmark information, that has been obtained from sources that GammaRoad believes to be reliable; however, such information has not been independently verified. GammaRoad (i) makes no representation as to, and accepts no responsibility or liability for, the accuracy, truthfulness or completeness of the information; (ii) and does not represent it as accurate, true or complete; (iii) makes no warranty, express or implied regarding it; and (iv) shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use unless the waiver of such liability constitutes the waiver of any rights you may have under applicable federal or state laws.

The information in this presentation is current as of the date indicated and is subject to change or amendment. The delivery of this presentation at any time does not imply that the information contained herein is correct at any time subsequent to such date. GammaRoad undertakes no responsibility or obligation to revise or update this presentation and/or the opinions, statements, assumptions, analyses, assessments, projections, forward looking statements, similar statements and other views expressed in this presentation (collectively, the “Statements”). All Statements constitute only subjective views of GammaRoad, should not be relied on, and are subject to change without notice due to many factors, including fluctuating market conditions, and economic factors.